David Protein: Diving Deeper

The on-the-surface numbers do not tell the whole story

I thought I’d shift away from sports here and talk about the David protein bar, which has spiked in popularity in the past few months. Some background: Peter Rahal, founder and CEO of David, was the founder of RXBAR, which skyrocketed in a four-year span and was eventually sold in 2017 to Kellogg's for $600 million. Rahal has shown a great understanding of consumer sentiment. Back in the mid-2010s, energy products, even if they were higher in carbs or sugar, were popular. Now, this has shifted to consumers being interested in high-protein, low-sugar products, such as David.

Recently, David raised a $75 million Series A round, led by some notable investors like Greenoaks and Valor Equity Partners. One of the partners at Greenoaks stated that they believe that David has a product that breaks the tradeoff of consumers having to make a choice “between convenience, taste, and nutrition.”

Now, this is a fairly unprecedented number to raise for a CPG product. So, how should we think about the potential of the business? Let’s start by specifically focusing on the marketing behind this.

Tremendous (sometimes overzealous) marketing on David’s website

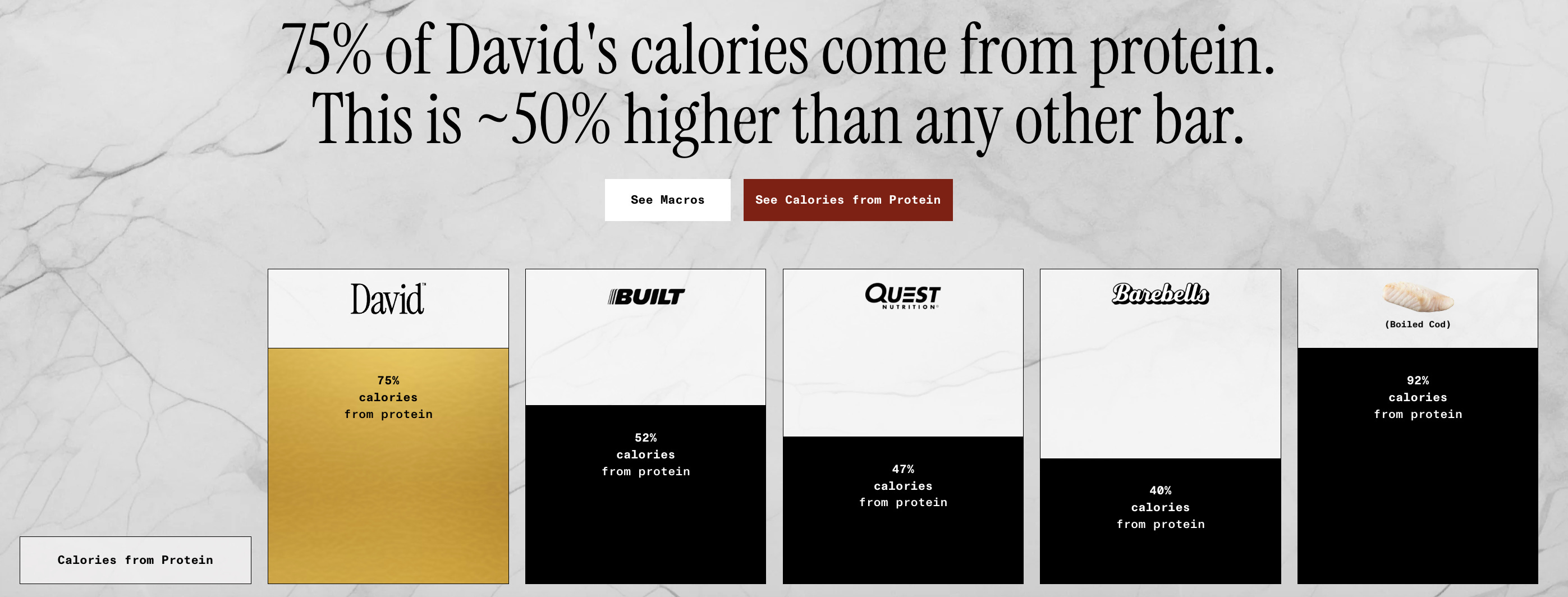

A key selling point David uses is that 75 percent of one bar’s calories come from protein, much higher than competitors.

This is tremendous marketing. For the consumer, the data point is easy to understand, and the small chart is intuitive as well.

On the bar itself, we also see three numbers listed: 28 grams of protein, 150 calories, and 0 grams of sugar. On the surface, this looks tremendous, and it fits with David’s mission. As Rahal states, their mission is “simple: to remove unnecessary calories and sugar from the American diet and replace them with what the body actually needs, which is high-quality protein.” There is no mention here about focusing on removing unnecessary ingredients, which brings me to the next part.

The ingredients are not very clean

When looking at the ingredient list for the David bar, it starts with the protein blend: milk protein isolate, collagen, whey protein concentrate, and egg whites. Nothing overly concerning here. Then, we move on to some of the other ingredients, such as maltitol, glycerin, allulose, and tapioca starch. The zero grams of sugar is technically true, but not very accurate. We see artificial sweeteners such as sucralose in this, and we also see “natural and artificial flavor,” which to me, as a consumer, is never a great sign. David also switched from using stevia and monk fruit to sucralose and acesulfame potassium relatively recently. It’s likely that these ingredient changes happened for the sake of lowering costs, even this early in the company’s journey.

In addition, there’s an ingredient called “modified plant fat,” also known as EPG. As an interesting side note, a key growth accelerator for David has been the fact that, at around the same time the Series A was announced, it also announced that it had bought the producer of EPG, a company called Epogee. David now has exclusive access to EPG, in the process hurting many other CPG companies who have been using this product. David may see access to EPG as a key source of advantage, and it’s possible that this was a part of the use of funds for the Series A. EPG is FDA-approved as “Generally Recognized as Safe,” but again, for many consumers, having something called modified plant fat as an ingredient is not ideal.

In all, there are 17 different ingredients in this bar. To state the obvious, David will not lead with this fact in its marketing anytime soon.

So, is it convenient? Yes. Does it taste good? From the few bites I had, I think it’s pretty solid. Is it nutritious? Not really.

This serves as a good reminder of how numbers should be seen as a data point and never the absolute truth. Kyle McCord having the most passing yards in college football last season didn’t automatically make him the best college quarterback. And in addition, the David bar having 0 grams of sugar does not automatically make it nutritious.

Obviously, this does not matter as much in terms of venture investing. The point below most definitely does (and rightfully so).

A proven founder moves the “confidence interval”

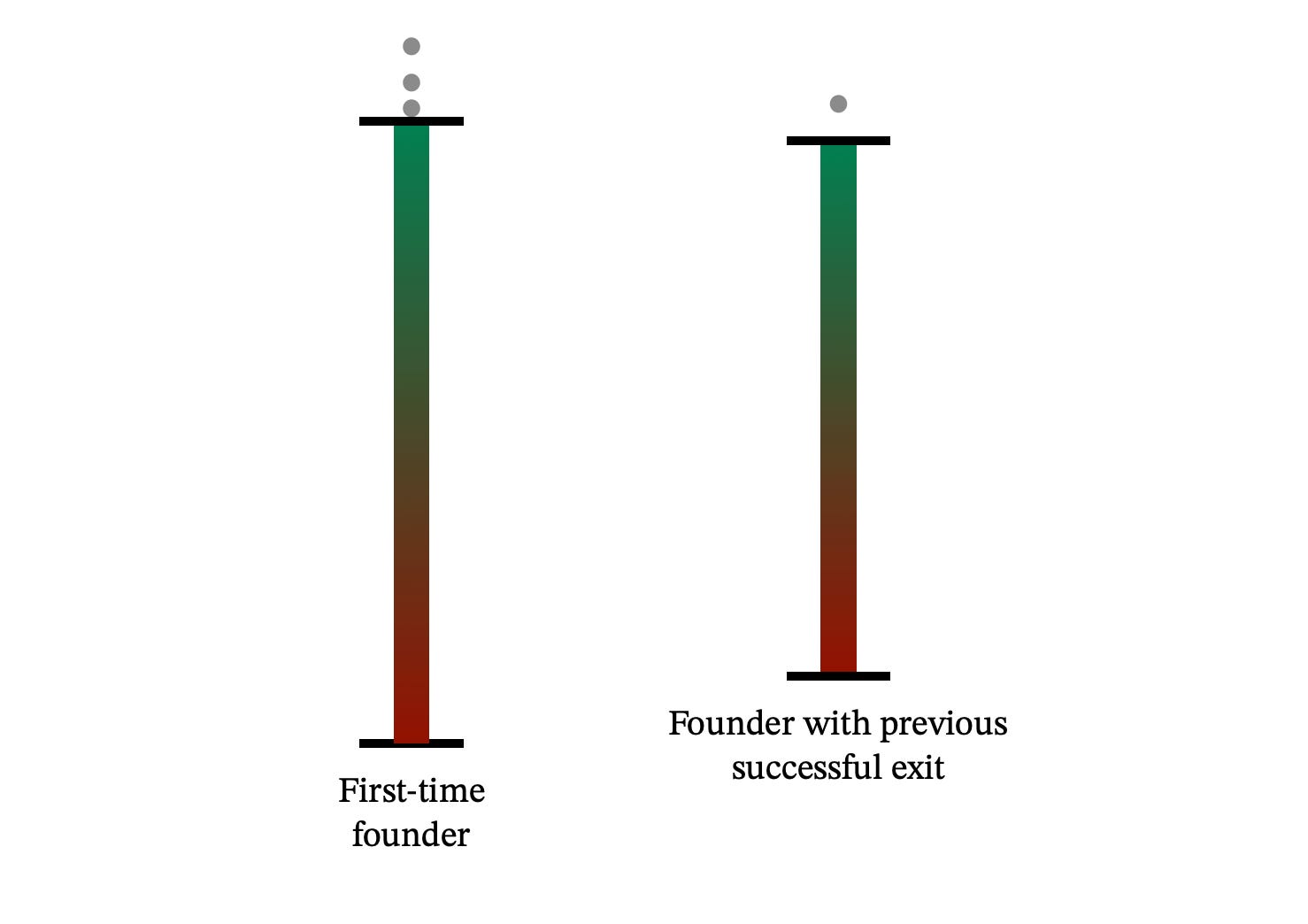

This is somewhat obvious, but from an investor’s point of view, when they’ve seen someone who’s already had a successful exit give another go at it, chances are they’re going to at least take a look.

In the case of David, Rahal’s RXBAR was sold to Kellogg's for $600 million in 2017 (as mentioned earlier).

When we have this data point, in probabilistic terms, the average low-end outcome improves. On the other hand, maybe the average high-end outcome decreases (less outliers, but with more certainty). So, the ceiling is not necessarily lowered; rather, the expected return is more predictable. One way of visualizing it is a bit like a confidence interval.

Too high a Series A?

Theoretically, a $75 million Series A seems like a bit much, especially in a sector where it is easy to switch between different products (i.e., lower switching costs).

For me, this ease of switching has felt very true as I’ve tried different hydration products. A few years ago, I switched from using Nuun to using Liquid IV. I wanted a powder instead of a tablet and something that was slightly sweeter. Around a year ago, Liquid IV changed its ingredients, and it started tasting much more artificial. So, I decided to look around Instagram and found a few other brands to try, from LMNT to Cure Hydration, and even re-considered Nuun. In today’s era of marketing through social media, it’s easy for the average consumer to come across companies like David, but it’s also easy to find other ones. And what if consumers keep focusing more and more on simple ingredient lists?

Circling back to Liquid IV, these ingredient changes happened not too long after Unilever acquired them for roughly $500 million. So, they had carved out enough of a presence to be acquired for that large sum.

The only way David’s high Series A can be justified is by making the assumption that they will be acquired by someone at a high price (so not if, but when), one even bigger than the $600 million Kellogg’s paid for RXBAR. Given the early traction, this could definitely happen. But as I think more about the differences between David and RXBAR, one thing in particular stands out. When you pick up an RXBAR at a store, you immediately see what’s in it on the front of the label, while with David, the macros (the key selling point) are slightly hidden, and the ingredients are not front and center.

This sets up an interesting question. Was the success of RXBAR based more on its clean and simple ingredients, or on innovative marketing? David seems to present an offering that tilts more towards the latter. Can this value proposition remain durable? Will a proven founder get David over the finish line? Or will it suffer something like what has happened to the sports drink Prime in recent months? This will definitely be an interesting one to watch.

As always, feel free to reach out via email (ryanajayholl@gmail.com) or through LinkedIn.